New report says half NRs residents face insurance stress

Simon Mumford

29 August 2024, 9:00 PM

A new report published by the Actuaries Institute this week reinforces what homeowners in Lismore and the Northern Rivers have known for the last twelve months: that house insurance is unaffordable.

Steeper home insurance premiums have caused the number of Australian households experiencing home insurance affordability stress to rise by 30% to 1.6 million in the past year, the report showed. It states that more than half of households in Lismore and the Northern Rivers face home insurance premiums that exceed a month's gross household income.

The Home Insurance Affordability and Home Loans at Risk Report found these households spend an average of 9.6 weeks of their gross income on home insurance, which is seven times more than the average household.

Overall, the proportion of “affordability stressed” households – those facing home insurance premiums that are more than one month’s gross annual income – rose to 15% in the year to March 2024 from 12% the previous year. The report, commissioned by the Actuaries Institute and authored by Finity actuaries, said affordability pressures had worsened following a 9% rise in median insurance premiums. Properties facing the 5% of highest premiums, typically due to floods and cyclones, endured the steepest rise in premiums, up by more than 30%.

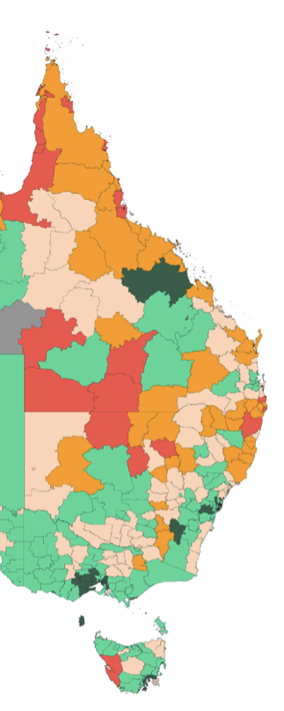

(Geographic Distribution of Home Insurance Affordability Pressure. Lismore in red and classified as extreme pressure 4+ weeks)

"The affordability pressures faced in these regions is typically driven by their high perils risk exposure, cyclone for northern Australia and flood for New South Wales.

The report’s lead author, Sharanjit Paddam, said, “While insurance remains generally affordable for 85% of households, it’s concerning that there’s now 1.6 million households struggling to afford to insure their homes, up from 1.24 million a year ago.

“This is because increases in premiums are outpacing wages growth. Unfortunately, we expect this will continue because of the overall increasing risk of natural disasters associated with climate change, which will continue to put upward pressure on premiums.”

The figures for the rest of NSW show that 83% do not have insurance affordability stressed households while 17% do. So, the majority of the state does not have the same financial insurance concerns that the Northern Rivers does.

In numbers, unstressed households in NSW pay around $2,200 per year, while stressed households are paying around $4,200 per year. That is 91% higher than unstressed households.

On an Australia-wide basis, perils costs make up 30% of mean annual insurance premiums for affordability-stressed households, compared to only 21% of non-stressed households. For 32% of affordability-stressed households, over half of the premium relate to perils costs, moslty from exposure to floods.

Affordability-stressed households pay, on average, at least 40% more than non-affordability-stressed households in all states other than the ACT and NT, in Western Australia the premiums for stressed household are more than double.

The most significant driver of affordability stress is exposure to flood risk. The image below shows that, at an Australia-wide level, flood premiums are 2% of premiums for non-stressed households but 15% of premiums for affordability-stressed households. At an Australia-wide level, the average flood premium paid by stressed households is nearly 16 times higher than that paid by non-stressed households (noting that flood risk only impacts around 7% of the Australian population).

A lot of households are now uninsured or underinsured. Underinsured due to the increase in building costs, approximately 15% over the last two years for building material and labour costs. The report said that the change in median retail prices at March 2024 was 15% in NSW.

The result of the above is that home loans are at risk due to affordability pressures.

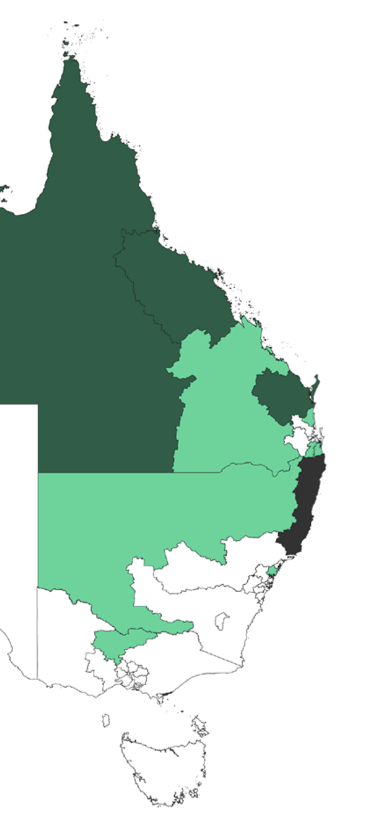

The report estimates that 5% of households in Australia with home loans are experiencing extreme home insurance affordability pressures, and that these households have $57 billion in loan balances outstanding as at March 2024 (home loans at risk), representing 3% of all home loan assets. Some of these properties also act as security for SME (Small Medium-sized Enterprises) commercial loans, which is not included in the analysis.

It was noted that some lenders do not require proof that home insurance is ongoing, so there could well be cases of homeowners paying of home loans that do not have home insurance.

The report says that large lenders have undertaken climate physical risk assessments and used the Commonwealth Bank of Australia’s Climate Report in 2023 (CBA, 2023) as an example. The report revealed approximately 32,000 properties, with mortgages worth $11 billion, have been assessed as having a high risk of exposure to cyclones, while 39,000 properties ($17 billion) are at risk of floods and 4,000 ($2 billion) at risk of bushfire. Overall, 4.6% of the bank’s home loan portfolio has been classified as high risk to one or more perils.

"This is potentially a problem that’s bigger than just insurance. It’s also a problem for lenders, regulators and governments," the report says.

"The risks for them are only going to rise as we face more climate-related natural disasters and increasing issues with insurance affordability.” The Actuaries Institute is encouraging governments, insurers, lenders and investors to collaborate on sustainable finance measures such as resilience loans and bonds.

Actuaries Institute CEO Elayne Grace said: “We know as a country we need to manage the risk of the changing climate. Sustainable finance should be part of the solution. It creates a path forward for households, investors, insurers and lenders, and allows government to focus on households in most need and community-level measures.”

If we know what the problem is, the question is, how long will it be until we have a solution?

You can read the full report here.